In today's fast-paced world, understanding how to fill out a temporary check is an essential skill that can save you from unnecessary hassles. Temporary checks are often used when you open a new bank account and are waiting for your official checks to arrive. They may not appear as formal as your personalized checks, but they serve the same purpose and are a convenient way to manage your finances in the interim. This guide aims to provide a comprehensive understanding of temporary checks, how to fill them out correctly, and their place in modern banking practices.

Temporary checks, though plain in appearance, carry significant weight in financial transactions. They can be a lifeline when you need to pay a bill, rent, or make a purchase, and your personalized checks are not yet available. However, many people are not familiar with how to correctly fill them out, leading to potential errors that could result in bounced checks or delays in payment processing. Understanding the nuances of temporary checks can prevent these issues and ensure smooth financial transactions.

By the end of this article, you will gain a clear understanding of how to fill out a temporary check, the different components involved, and tips to avoid common mistakes. We will walk you through each step with detailed explanations and provide insights into how you can effectively use temporary checks until your official ones arrive. Let's delve into the world of temporary checks and enhance your financial literacy with this essential skill.

Table of Contents

- Understanding Temporary Checks

- Components of a Temporary Check

- Step-by-Step Guide to Filling Out a Temporary Check

- Writing the Date

- Filling in the Payee Information

- Writing the Amount

- Signing the Check

- Keeping Records

- Avoiding Common Mistakes

- Advantages and Limitations of Temporary Checks

- Temporary Checks vs. Personal Checks

- Security Concerns with Temporary Checks

- Frequently Asked Questions

- Conclusion

Understanding Temporary Checks

Temporary checks are often provided by banks when a new account is opened, serving as a stopgap measure until personalized checks are available. These checks are usually quite basic, lacking the customized features of standard checks, such as your name or address. Despite their simplicity, they are fully functional and can be used much like regular checks for various transactions.

One of the key characteristics of temporary checks is their anonymity. Since they don't carry personal details, they can be a bit more secure in terms of privacy. However, this also means that the user must fill them out meticulously to ensure the bank processes them correctly.

Temporary checks are especially useful in situations where immediate financial transactions are necessary. They serve as a critical tool in maintaining the flow of funds when personalized checks are delayed or when you’re waiting for them to be delivered. Understanding how to fill out a temporary check properly is crucial to avoid any disruptions in your financial activities.

Components of a Temporary Check

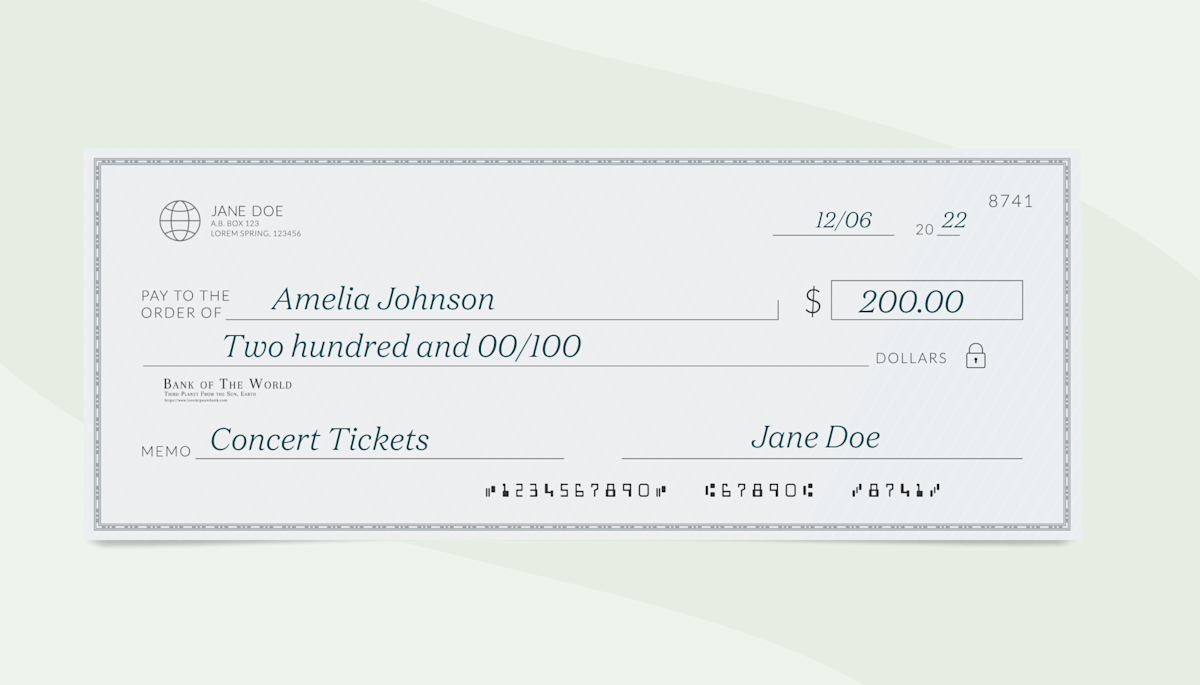

Though temporary checks may seem sparse compared to personalized checks, they still contain the essential components needed for completing a financial transaction. Here are the main parts you will find on a temporary check:

- Bank Information: This is typically pre-printed and includes the bank's name and sometimes its logo.

- Check Number: Usually located at the top right corner, this number helps keep track of each check and is essential for record-keeping.

- Routing Number: Found at the bottom left, this number identifies the bank and is crucial for processing the check.

- Account Number: Located next to the routing number, this identifies your specific account and is vital for directing the funds correctly.

While these are the basic elements, understanding each component's purpose helps ensure that you fill out the check accurately. Each element plays a specific role in the transaction process, allowing banks to process and clear the checks efficiently.

Step-by-Step Guide to Filling Out a Temporary Check

Filling out a temporary check might seem daunting at first, especially if you're unfamiliar with the process. However, by following a structured approach, you can fill it out correctly and efficiently. Here's a detailed step-by-step guide:

Each of these steps is critical in ensuring that the check is completed correctly and can be processed without any issues. Let's explore each step in detail.

Writing the Date

The date is one of the most important elements of a check. It indicates when the check was written and is critical for record-keeping and processing. To fill out the date, locate the date line usually found in the top right corner of the check. Write the current date in a clear and legible manner using the format MM/DD/YYYY or DD/MM/YYYY, depending on your preference or the country's standard format.

It's important to ensure that the date is accurate, as post-dating or pre-dating a check can lead to confusion and potential delays in processing. The date also plays a crucial role in determining when the funds will be withdrawn from your account, so it must be correct to avoid any discrepancies with your bank balance.

Filling in the Payee Information

The payee is the individual or business to whom you are writing the check. Filling in this section accurately is essential to ensure that the correct party receives the funds. Locate the line that says "Pay to the Order of" and write the full name of the payee. Avoid using nicknames or abbreviations, as these can lead to issues with cashing or depositing the check.

If you're writing the check to a business, include the full legal name of the company. For individuals, using the full name as it appears in official records is best. This step helps prevent any confusion or disputes over the rightful recipient of the funds.

Writing the Amount

Writing the amount on a check involves two areas: the numerical box and the written line. Both must be completed accurately to avoid any issues with processing.

First, in the box provided, write the amount of the check in numerical form. Be sure to write clearly and avoid any ambiguous figures that could be misinterpreted. It's also a good practice to start writing the amount from the far left of the box to prevent any unauthorized alterations.

Next, write the amount in words on the line below the payee's name. This step is crucial as it serves as a backup for the numerical amount. If there's any discrepancy between the two, banks typically refer to the written amount. Ensure you use clear language and include "and" before the cents (e.g., "Thirty-three dollars and 45/100").

Signing the Check

Your signature is a critical component of the check, serving as your authorization for the bank to release the funds. Locate the signature line, usually found at the bottom right corner of the check. Sign your name in the same manner you have on record with the bank. A mismatched signature can result in the check being rejected or delayed.

It's important to ensure your signature is legible and matches the signature card on file with the bank. Any significant deviation might cause the bank to question the check's authenticity, leading to processing delays.

Keeping Records

Maintaining accurate records of your checks is essential for managing your finances effectively. After filling out a check, make a note of the transaction in your check register or financial tracking system. Include details such as the check number, date, payee, and amount. This practice helps you monitor your spending and ensures you have a record if any issues arise.

It's also beneficial to keep copies of filled-out checks, either physically or digitally, to refer back to if needed. This step is especially important for temporary checks, as they lack personal identification information, making it crucial to track them diligently.

Avoiding Common Mistakes

Filling out a temporary check correctly is crucial to avoid any financial hiccups. Here are some common mistakes to avoid:

- Incorrect Payee Name: Double-check the spelling and accuracy of the payee's name to prevent any issues with cashing or depositing the check.

- Mismatched Amounts: Ensure the numerical and written amounts match to avoid disputes or delays in processing.

- Illegible Writing: Write clearly and legibly, especially in the payee and amount sections, to prevent any misunderstandings.

- Missing Signature: Always sign the check before handing it over to ensure it is valid and can be processed without delays.

By being mindful of these common pitfalls, you can ensure that your temporary checks are filled out correctly and processed smoothly. This attentiveness not only facilitates transactions but also enhances your credibility in financial dealings.

Advantages and Limitations of Temporary Checks

Temporary checks offer both advantages and limitations compared to personalized checks. Understanding these can help you decide when it's appropriate to use them.

Advantages

- Immediate Availability: Temporary checks are often available immediately when opening a new account, allowing you to make transactions without waiting for personalized checks.

- Cost-Effective: They are typically provided for free or at a low cost, making them an economical option for short-term use.

- Privacy: Since they do not contain personal information like your name or address, temporary checks offer a degree of privacy in transactions.

Limitations

- Lack of Personalization: Temporary checks lack standard features like your name or address, which can sometimes lead to confusion or require additional verification.

- Limited Quantity: Banks usually provide a limited number of temporary checks, which may not suffice for frequent transactions.

- Perceived Lack of Professionalism: Temporary checks may be perceived as less professional, especially in business transactions, due to their plain appearance.

Despite their limitations, temporary checks are a valuable tool for managing finances during the interim period when personalized checks are not available.

Temporary Checks vs. Personal Checks

Understanding the differences between temporary and personal checks can help you make informed decisions about their use.

Temporary Checks

- Issued at the time of opening a new account

- Lack personal details such as name and address

- Used for short-term, immediate transactions

- Typically provided in limited quantities

Personal Checks

- Customized with personal details and often a unique design

- Used for long-term banking needs

- Generally perceived as more professional

- Typically ordered in bulk

Each type of check serves specific purposes and offers unique benefits and drawbacks. Understanding these differences can help you choose the right check for your financial needs.

Security Concerns with Temporary Checks

While temporary checks are a useful financial tool, they do come with certain security concerns that users should be aware of. One primary concern is their lack of personalization, which can sometimes lead to fraudulent activities if not handled carefully. Here are some tips to enhance security:

- Keep Checks Secure: Store temporary checks in a safe place to prevent unauthorized access or theft.

- Monitor Accounts Regularly: Regularly check your account statements to detect any unauthorized transactions promptly.

- Shred Used Checks: Once a temporary check is processed and no longer needed, shred it to prevent misuse of your account details.

By taking these precautions, you can minimize security risks associated with using temporary checks and ensure your financial information remains protected.

Frequently Asked Questions

1. Can I use a temporary check for online payments?

Temporary checks are typically not suitable for online payments because they lack the personalization and security features required for digital transactions. It's best to use other payment methods, such as debit cards or online banking, for online purchases.

2. How long can I use temporary checks?

Temporary checks are intended for short-term use, usually until your personalized checks arrive. The exact duration depends on your bank's policies and the time it takes for personalized checks to be delivered.

3. Are there any fees associated with temporary checks?

Most banks provide temporary checks for free or at a minimal cost when you open a new account. However, it's advisable to check with your bank for specific details regarding any potential fees.

4. Can I order more temporary checks if I run out?

Typically, banks provide a limited number of temporary checks, and it may not be possible to order more. If you run out, consider using alternative payment methods or wait for your personalized checks to arrive.

5. Do all banks offer temporary checks?

Most banks offer temporary checks when you open a new account, but it's best to confirm with your specific bank to ensure they provide this service.

6. What should I do if a temporary check is lost or stolen?

If a temporary check is lost or stolen, contact your bank immediately to report the issue and prevent unauthorized use of your account. They can guide you on the necessary steps to secure your account and replace the lost checks.

Conclusion

Understanding how to fill out a temporary check is an invaluable skill that can aid in managing your finances efficiently. Temporary checks are a practical solution for interim banking needs, providing a way to conduct transactions while waiting for personalized checks. By following the step-by-step guide outlined in this article, you can fill out a temporary check correctly and ensure a smooth transaction process.

While temporary checks come with certain limitations and security concerns, being aware of these issues and taking appropriate precautions can mitigate potential risks. By maintaining accurate records, avoiding common mistakes, and understanding the differences between temporary and personalized checks, you can use temporary checks confidently and effectively.

As you navigate the world of temporary checks, remember that they are a temporary tool designed to serve your immediate financial needs. Once you receive your personalized checks, you can transition to using them for more formal and long-term banking purposes. This knowledge empowers you to make informed decisions about your financial transactions and enhances your overall financial literacy.

For further reading on banking practices and financial management, you may find resources provided by the Consumer Financial Protection Bureau helpful. They offer a wealth of information on managing personal finances and understanding banking products.

You Might Also Like

How To Apply Foundation To Mature Skin: Expert Tips And TechniquesThe Enigmatic Power Of Batman's Strongest Suit

Understanding The Difference Between Sarcastic And Sardonic: A Comprehensive Guide

Casual Parties: The Ultimate Guide To Hosting And Attending

The Mysterious Tale Of Anne Boleyn's Ghost: A Journey Through History And Legend

Article Recommendations

- Bat House For Garden

- What Does Inexplicable Mean

- Ubuntu Install Deb File Command Line

- Enoch In Spanish

- Whats The Best Water For You

- Gold Piercing Helix

- Biomedical Science

- Malachi Bush

- Liam Payne Picture

- Raquel Pedraza